Equities extend their all-time highs. The SPX rose 0.22% to end the day at 4,850 ahead of a packed earnings calendar this week. Stocks have largely rebounded after a sluggish start to 2024, driven by renewed tech optimism and the AI boom. Netflix and Tesla announce earnings tomorrow, the former expected to benefit from its password-sharing crackdown and the latter expected to announce strong quarterly sales but a ~38% drop in EPS from a year ago. Meanwhile, rates were little changed today as markets await upcoming PCE inflation figures.

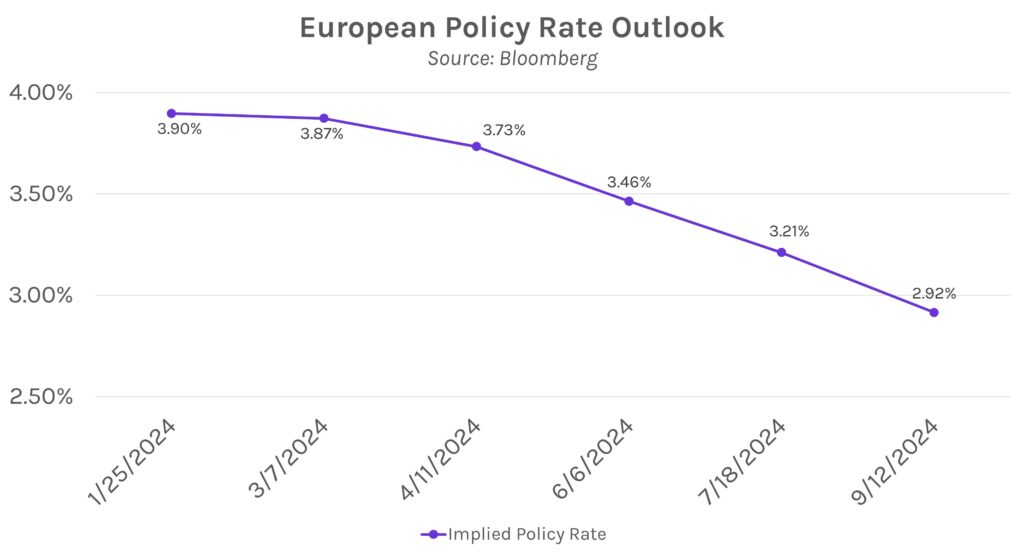

Uncertainty persists in Europe ahead of January 25th ECB meeting. Though core price inflation fell from ~6.60% in March 2023 to ~3.96% in December 2023 on a YoY basis, markets have been more conservative about pricing in Eurozone policy easing vs. in the US. The EU is seeing strong wage growth and record low levels of unemployment, even as the economy appears on track for a recession following negative real GDP growth in 3Q23. Futures markets largely expect the ECB to hold the policy rate at 4.00% this week, with the first cut appearing in April, but ECB president Lagarde said at Davos last week that wage growth could have a “serious impact” on the ECB’s plans. She wants to wait for 2024 salary data released in late spring before lowering the policy rate, implying rate cuts may not happen until the summer.

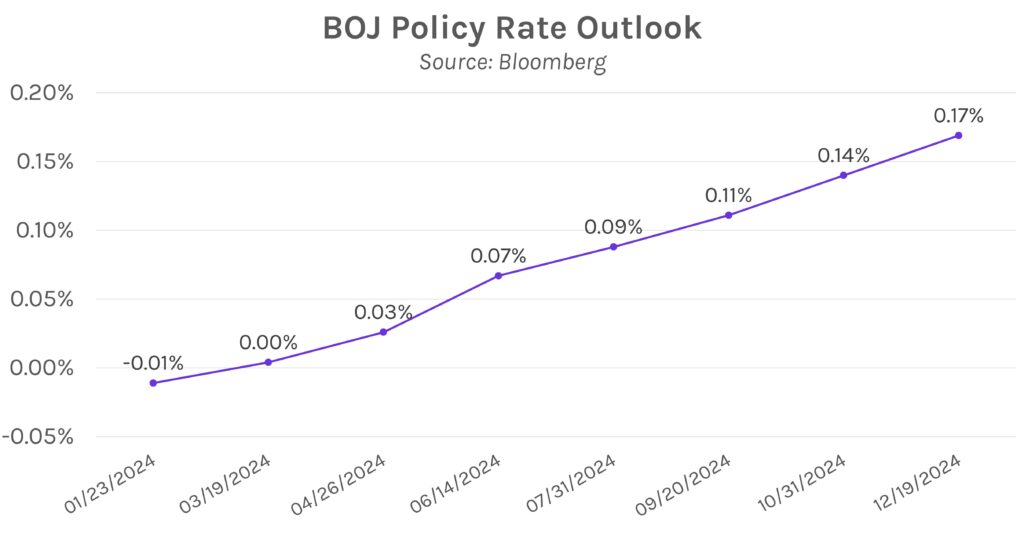

Bank of Japan expected to hold policy rate at -0.1%. The BOJ will announce its policy decision tomorrow, where markets largely expect short-term rates to be held at -0.1%. Though a hike is unlikely until at least April, markets will peruse Ueda’s comments on progress toward sustained inflation and wage growth. CPI inflation was 2.3% YoY in December, the lowest since June 2022. However, Japanese employers are expected to raise wages significantly in 2024, which could fuel a BOJ pivot away from negative rates.