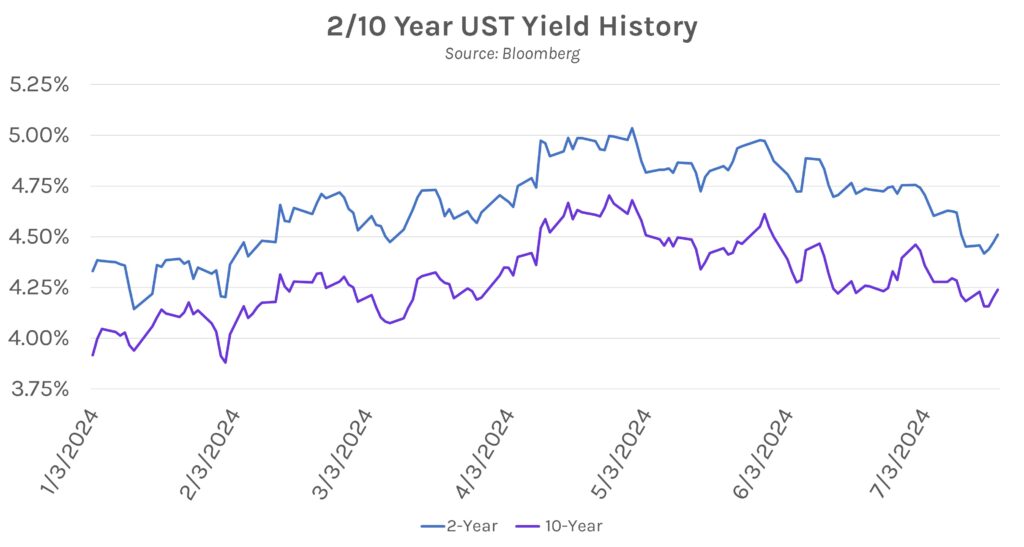

Rates continue their gradual climb while big tech finishes the week with another sell-off (and blackout). Swap rates rose 3-5bps today and are now ~10bps higher from the week’s lows, which were reached on Tuesday. The 2y Treasury yield closed the week just over 4.51% while the 10y yield is at 4.24%. That puts the 2s10s inversion at only ~27bps, just 5bps from the steepest yield curve since January. Meanwhile, equities largely continued to struggle as the S&P 500 closed out its worst week since April. Big tech was the headliner for poor performers, especially after last night’s system outages wreaked havoc across the globe. Hopefully this piece makes its way into your inbox!

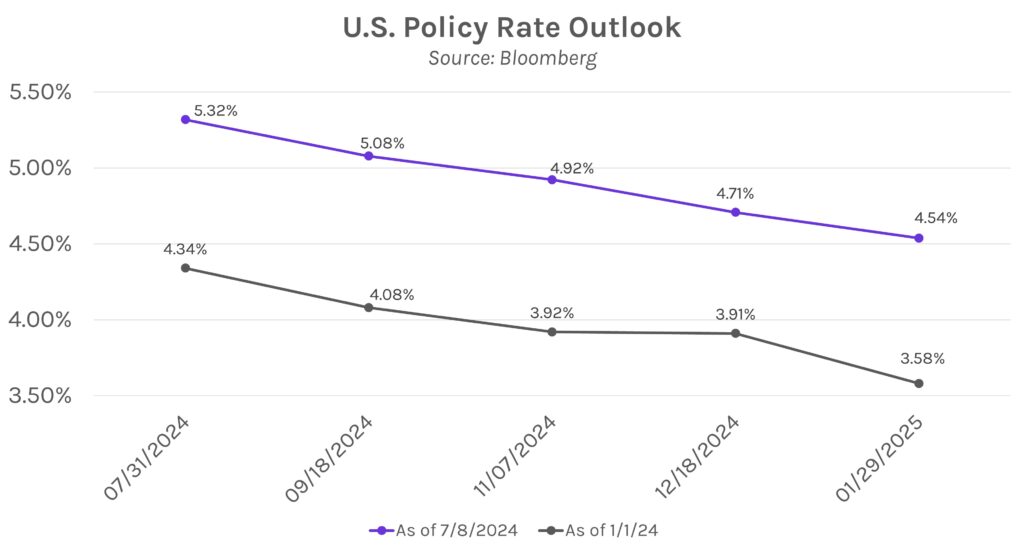

Fed President Williams sees lower long-term neutral rate. Despite various inflationary pressures over the past few years stemming from choked global supply chains, domestic fiscal stimulus and other measures, Williams said at a panel today that his estimates of the neutral rate in the U.S, Canada and Eurozone are roughly in-line with pre-pandemic levels. He added that forces supporting low rates pre-pandemic are “still very much intact.” This follows the Fed’s projections in June showing they believed the neutral rate rose from 2.5% pre-pandemic to ~2.8%.

Inflation data looms in the week ahead. Next week’s slate will be headlined by personal consumption expenditures (PCE) data, the Fed’s preferred gauge of inflation. Core PCE is expected to extend its multi-year lows to 2.5% from 2.6%, a positive sign for doves after recent consumer price data showed signs of slowing inflationary pressures. Advanced Q2 GDP data (set for release on Thursday) is expected to show a jump to 1.9% from 1.4% in Q1.