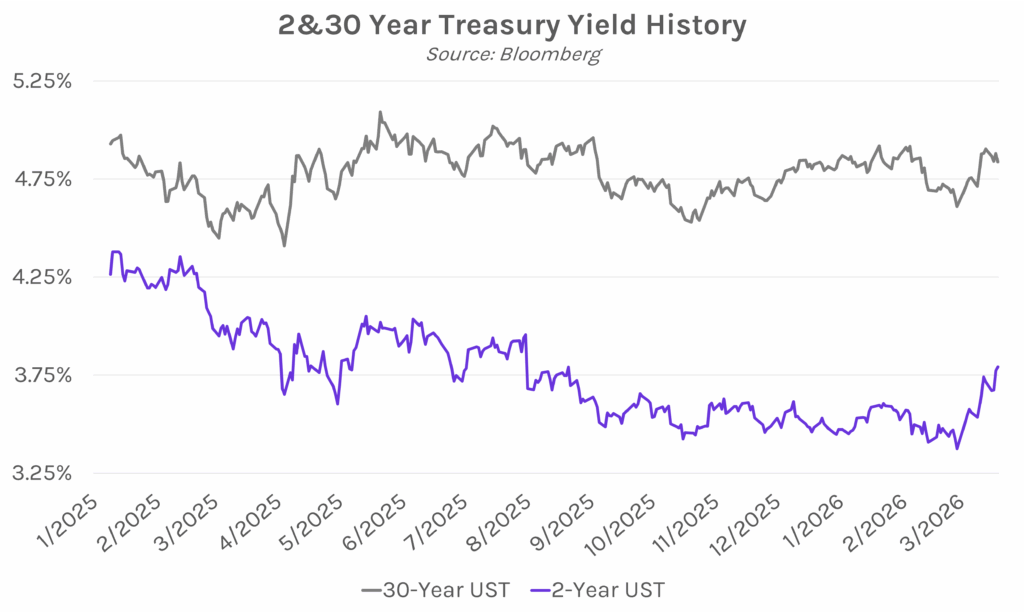

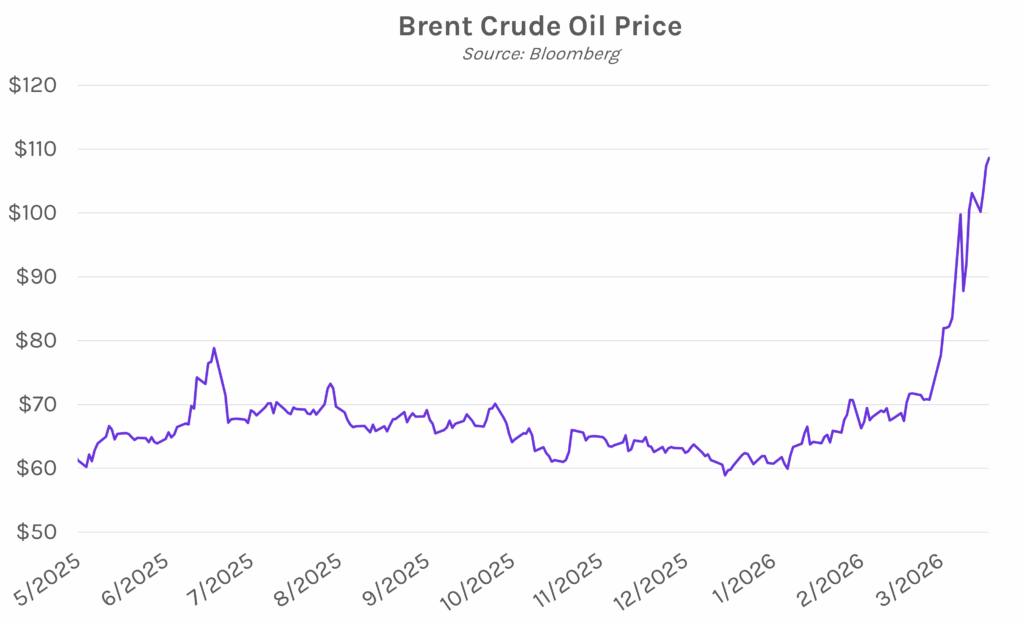

Yields mixed on volatile oil prices. Treasury yields soared 5-15 bps this morning as oil prices surged following attacks on an energy facility in the Middle East. Expectations of 2026 rate hikes from the ECB and BOE also drove rates movement. Yields whipsawed over the remainder of the session, with the 2-year yield ultimately closing 2 bps higher at 3.79%, and the 30-year yield 4 bps lower at 4.84%. Meanwhile, equities fell today, with the S&P 500 and NASDAQ closing 0.27% and 0.28% lower, respectively.

Oil volatility persists as Middle East conflict rages on. Early on Thursday, Israeli missiles struck the world’s largest liquified natural gas plant in Qatar. The CEO of Qatar Energy, Saad al-Kaabi said the damage would take three to five years to repair. Although Israeli Prime Minister Netanyahu said his country would hold off on further strikes on energy facilities, the remarks did little to quell market concerns. President Trump also downplayed Iran’s attacks, saying “it’s not bad, and it’s going to be over with pretty soon.” Brent crude briefly topped $119 a barrel on the news, up 11% on the day, before closing above $108, while European gas futures jumped as much as 35%. Offering a small source of relief, the IEA announced details of their coordinated emergency crude oil releases, with Canada, Japan, and South Korea among the largest contributors.

ECB, BOE expected to hike rates in 2026. The European Central Bank voted to hold rates steady at 2% today, with President Christine Lagarde citing that the ECB is well positioned to deal with risks associated with the war in Iran. According to people familiar with the situation, ECB policymakers are ready to hike rates if inflation rises sharply due to surging oil prices from the war. Meanwhile, the Bank of England unanimously voted to leave rates unchanged at 3.75% today, the first meeting in over four years that had no dissenting votes. The BOE similarly remains focused on tackling inflationary impacts of the war, with Governor Andrew Bailey, a historic dove, saying that policy must “respond to the risk of a more persistent effect on UK CPI inflation.” Futures markets are now fully pricing in two rate hikes by the ECB and BOE this year.