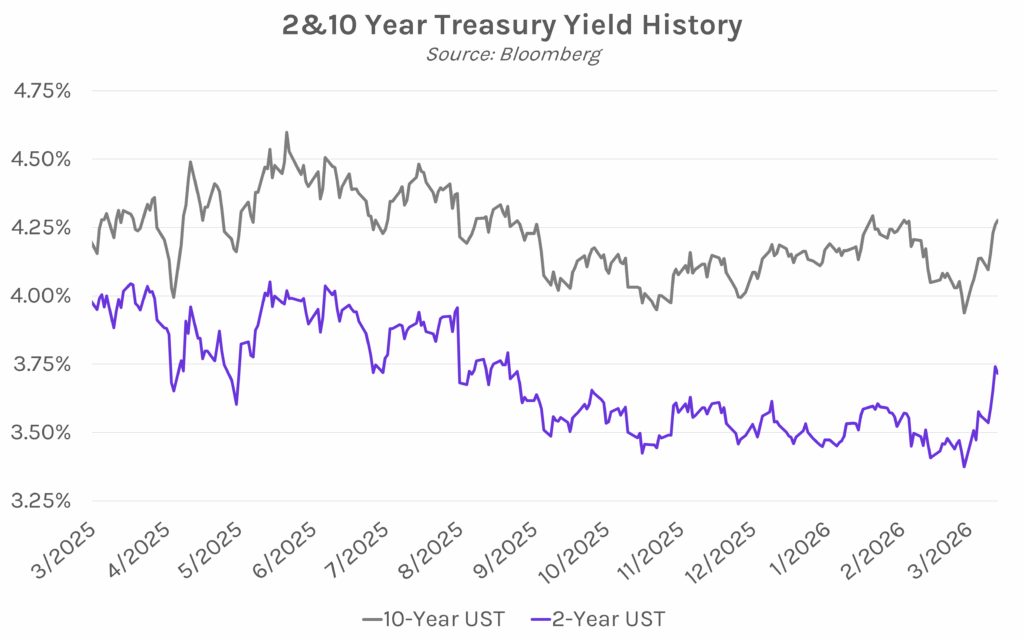

Yields mixed on sluggish economic data, elevated oil prices. Treasury yields declined this morning on tame PCE and consumer spending data, though price action reversed course shortly thereafter on rising oil prices. The 2-year yield closed 2 bps lower at 3.72% (up 16 bps on the week), while the 10-year yield closed 2 bps higher at 4.28% (up 14 bps on the week). Crude futures are at the highest levels in over three years, with Brent closing above the $103 price level. Meanwhile, equities continued their selloff, with the S&P 500 and NASDAQ closing 0.61% and 0.93% lower, respectively.

Federal judge blocks DOJ subpoenas targeting Fed Chair Powell. In a filing today, Chief Judge James Boasberg, of the US District Court for Washington, D.C., said the government had “produced essentially zero evidence” of wrongdoing. The ruling added that there was “a mountain of evidence…that the Government served these subpoenas on the Board to pressure its Chair into voting for lower interest rates or resigning.” The ruling is the latest in a series of court decisions that have interfered with the White House’s efforts to influence the independence of the Federal Reserve. Meanwhile, Senator Thom Tillis (R-NC) has said he will block the confirmation of Kevin Warsh, Trump’s nominee to replace Powell, until the probe into Powell is dropped. After today’s decision released, Tillis posted on social media that “appealing the ruling will only delay the confirmation of Kevin Warsh as the next Fed Chair.”

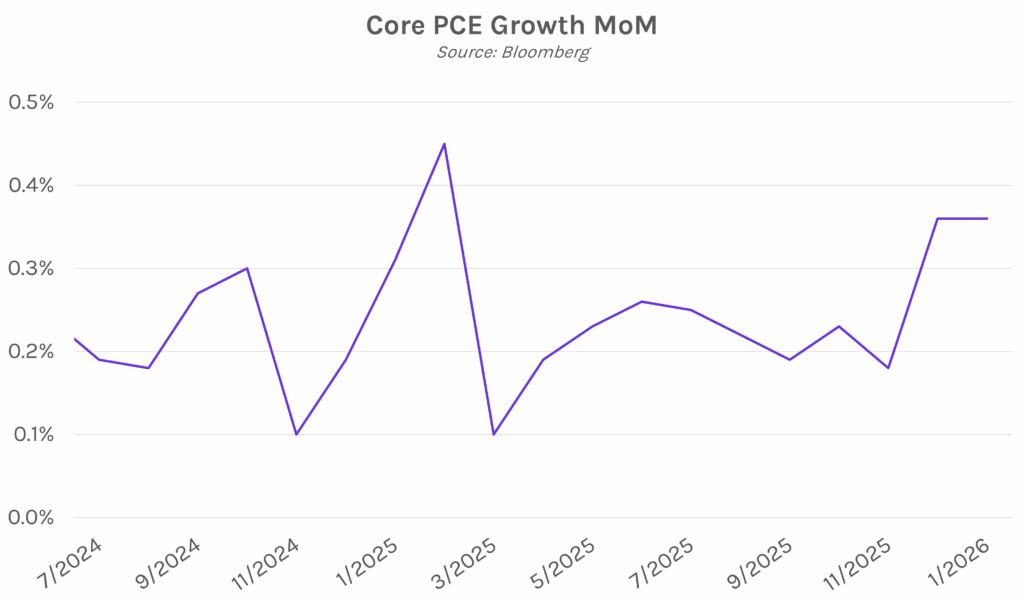

Core PCE remains elevated as consumer spending stalls. Core PCE, the Fed’s preferred inflation gauge, increased 0.4% in January compared to the month prior. Despite today’s PCE report largely coming in as expected, the war in Iran has driven energy prices higher in recent weeks, raising concern about potential inflationary impacts. According to Gregory Daco and Lydia Boussour, economists at EY-Parthenon, the conflict “is likely to leave a visible mark on the US economy through higher energy prices, tighter financial conditions, elevated private-sector uncertainty and renewed supply chain stress.” Consumers are expected to feel the impact, though pre-war data showed inflation-adjusted consumer spending rose 0.1% in January, a slight improvement against expectations of no increase. It’s anticipated that tax refunds and wage growth will help to support consumer spending in the coming months, however the full impact of war-related disruptions, and inflation, remain to be seen.