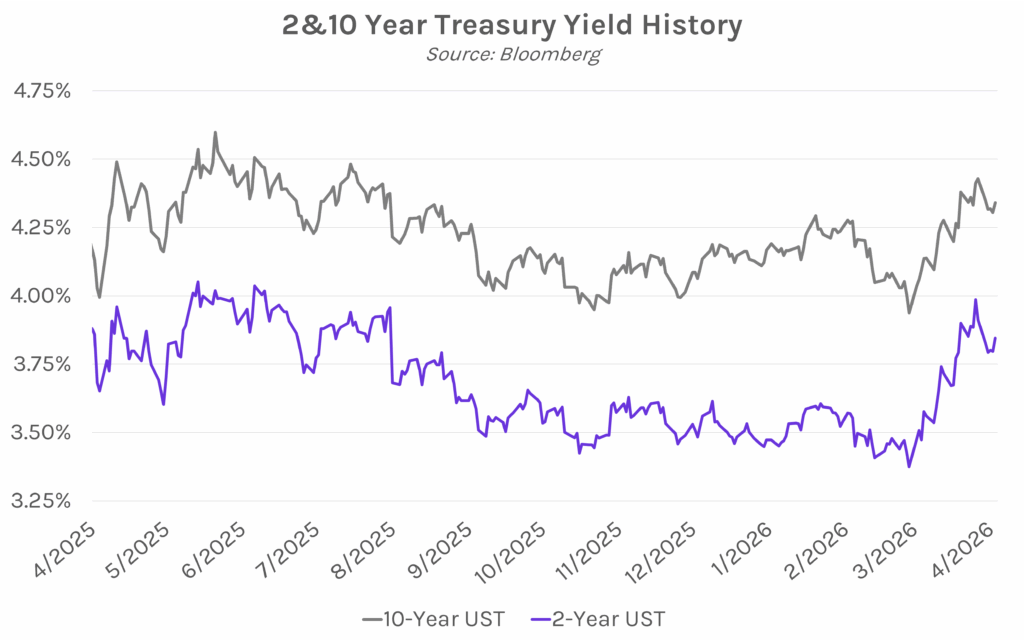

Yields climb on hot labor data. Treasury yields soared 5-6 bps in the immediate aftermath of strong March labor data, which showed robust hiring and a decline in the unemployment rate. The move partially reversed into the early market close, with the 2-year and 10-year yield closing 4-5 bps higher at 3.84% (down 7 bps on the week) and 4.34% (down 9 bps on the week), respectively. Focus will shift back to ongoing developments in the Iran War and next week’s inflation data, with February PCE being released on Thursday and March CPI on Friday. The CPI report will be one of the first looks into how the Iran War has impacted inflation in the US, with CPI MoM expected to increase 1%, up from 0.3% in February.

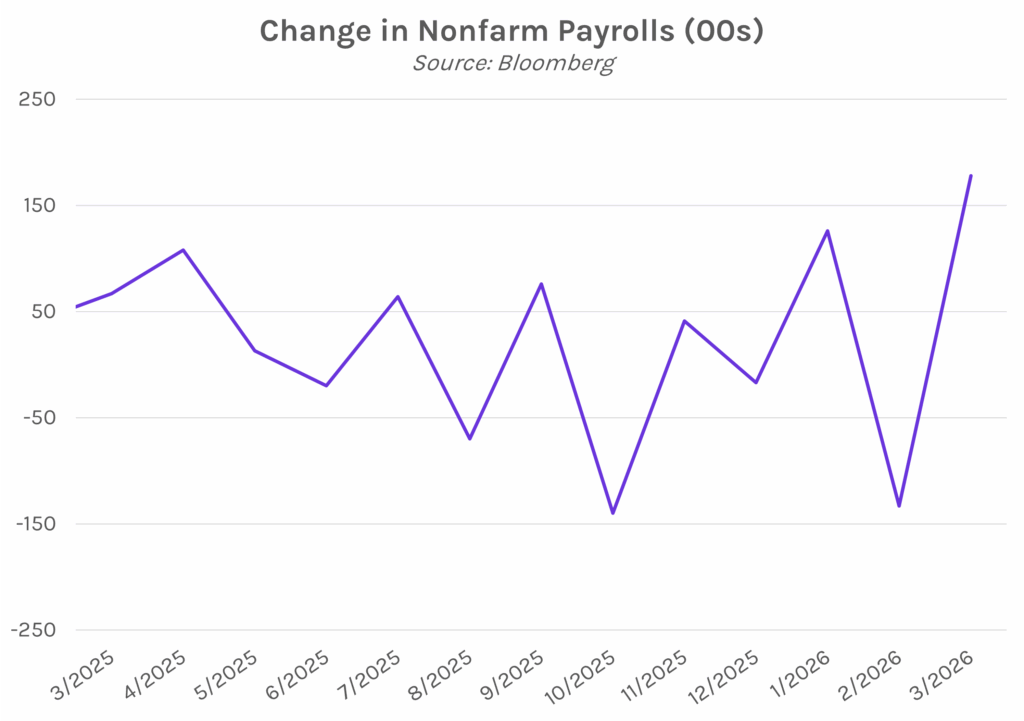

US labor market rebounds in March as unemployment rate falls. Nonfarm payrolls data showed 178k jobs added in March, well above estimates of 65k and reversing the prior month’s revised 133k decline. This marks the strongest monthly gain since 2024, led by hiring in the education and healthcare sectors, which rebounded as strike-related disruptions eased. Meanwhile, private payrolls increased by 186k, also exceeding forecasts of 78k and recovering from February’s 86k decline. The unemployment rate declined to 4.3% from 4.4%, reflecting the end of healthcare strikes and the impact of February’s severe winter weather. Overall, the strength of today’s BLS data will likely reinforce the Federal Reserve’s focus on inflationary risks amid the ongoing war in Iran.

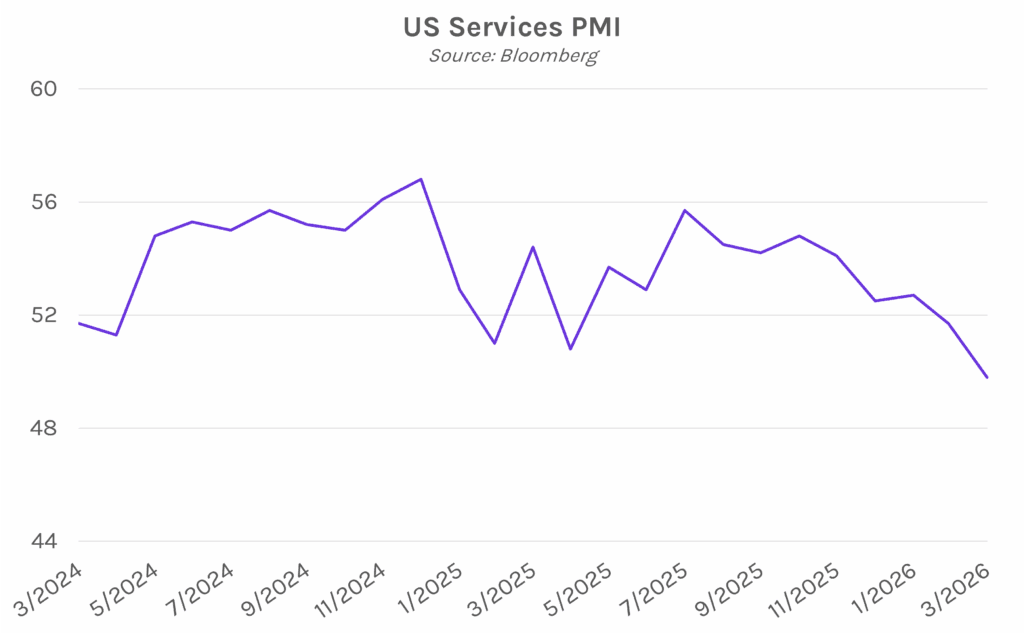

Services activity shrinks for the first time since 2023. The final March services PMI reading printed at 49.8, down from the preliminary reading of 51.1 and the first services activity contraction since 2023. Meanwhile, the input prices gauge rose to a three-month high, which resulted in higher prices for customers as companies passed along the costs. Chris Williamson, chief business economist at S&P Global, said, “Worst hit is consumer-facing services sectors where, barring the pandemic lockdowns, the downturn reported in March was among the steepest recorded since data were first available in 2009.” The composite index declined to 50.3 from 51.4 in the preliminary reading, largely driven by the decline in services activity.