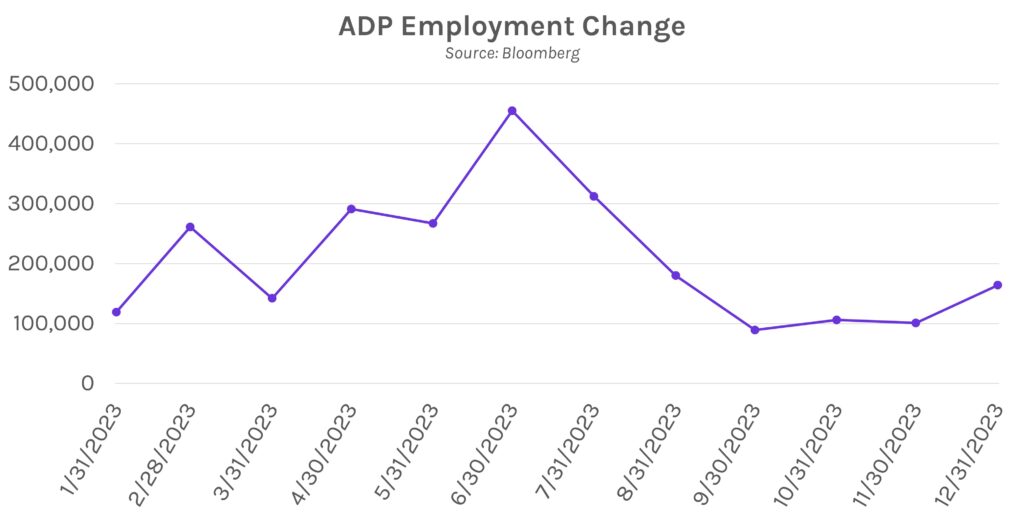

2024 bond and equity sell-off resumes ahead of tomorrow’s labor slate. Swap rates and Treasury yields have climbed since the year began, buoyed by today’s 5-8bps increase across the curve with the 10-year yield now at 4%. Strong US labor data (including ADP employment change) drove the move ahead of tomorrow’s nonfarm payrolls and unemployment rate figures. Ahead of tomorrow’s data, futures suggest a ~67% chance for the Fed’s first rate cut by the end of March’s FOMC meeting, a significant decline from over 100% a few weeks ago. Meanwhile, equities performed poorly, the SPX and Nasdaq 100 down for a 4th and 5th straight session, respectively.

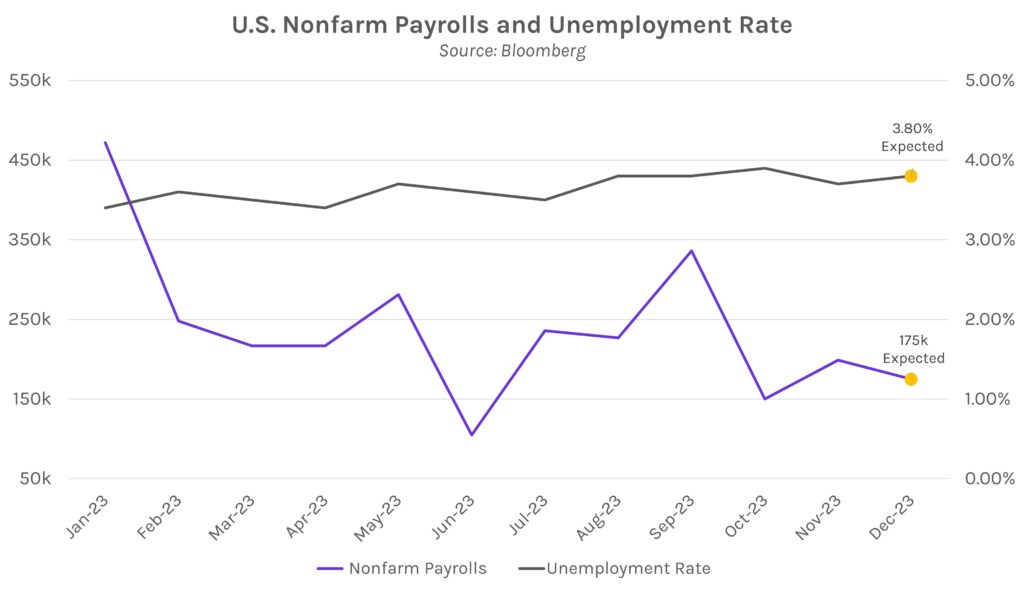

Markets hope for “goldilocks” results from tomorrow’s labor data. Nonfarm payrolls (NFP) growth trended downward from last May, but still increased by at least 150,000 per month from July to December. Similarly, the unemployment rate climbed throughout 2023, ranging between 3.4% – 3.9%, but remained in-line with 2019 levels. Tomorrow, markets will be focused on if December data builds on that “strong but cooling” trend. Whereas a high NFP print could undercut support for a March rate hike, a dramatically low figure could present concerns about the economy. Art Hogan, chief market strategist at B. Riley, believes the acceptable NFP range is between 100,000 – 250,000. Currently, markets expect a +175,000 NFP increase, ~14,000 less than November, and a 0.1% MoM increase in the unemployment rate to 3.8%. The government labor data will follow today’s private payrolls figure, which increased the most since last August, and yesterday’s job openings data that was below last month’s figures – both signs of strength.

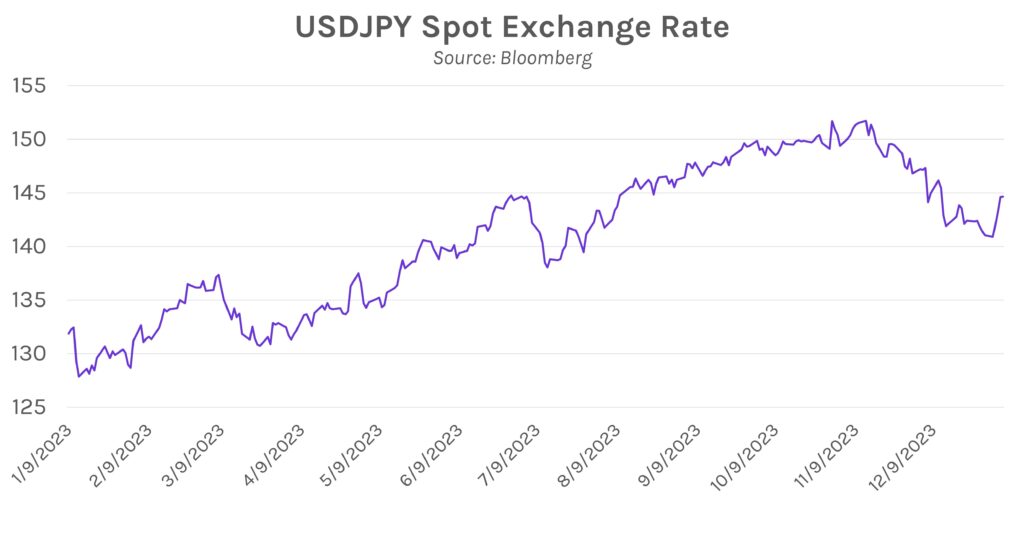

Japanese Yen under fire after New Year’s earthquake complicate BOJ policy decision. This week’s significant earthquake in Japan, which killed more than 80 people and forced thousands to evacuate, could limit economic activity and force the government to coordinate a supplementary budget for recovery measures. Speculation about the end of negative rates as early as this month faded as a result, driving a third consecutive decline in the Yen to nearly 145 per USD from 143 at the open. Though a January move is likely off the table, futures still see a strong likelihood (~56%) for a rate hike by the end of the April policy meeting.