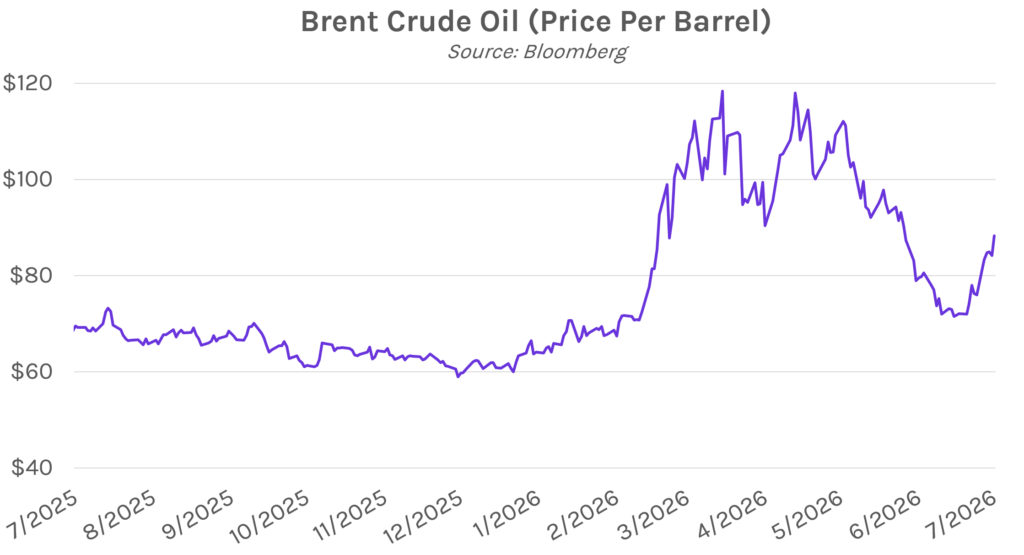

Yields mixed as US-Iran strikes continue. Treasury yields were mixed today as additional attacks between the US and Iran drove oil prices higher, pushing short-dated yields up and reversing the morning’s risk-off rally. The 2-year yield closed 4 bps higher at 4.18% (down 3 bps on the week), while the 10-year yield closed 1bp lower at 4.55% (down 1bp on the week). Brent crude closed at $88 per barrel, up over 16% from a week ago. Meanwhile, equities fell on continued selloff in semiconductor stocks, with the S&P 500 and NASDAQ closing 1.01% and 1.40% lower, respectively.

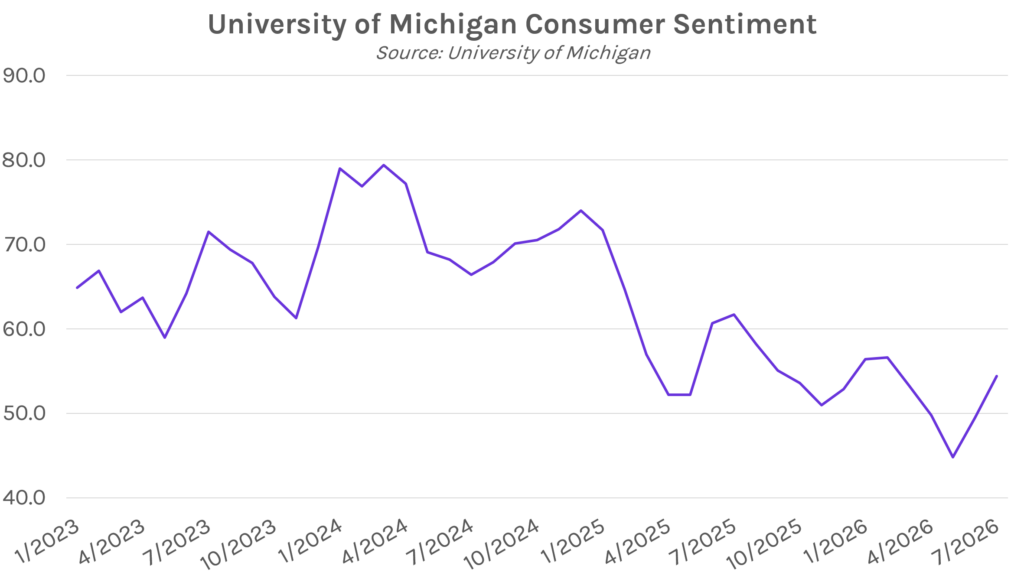

Consumer sentiment climbs as gas prices ease. The University of Michigan consumer sentiment survey hit 54.4 this month, well above June’s 49.5 reading and the highest posting since February. The improvement in sentiment was mainly driven by falling gas prices as the average US gallon of gas was $3.86 between June 23rd and July 13th, compared to $4.49 in May, according to AAA. Despite this, gas prices have recently increased as tensions in the Middle East have re-escalated and the Strait of Hormuz has largely closed to vessel traffic. Joanne Hsu, director of the Michigan survey states that these positive consumer sentiment results “may prove difficult to sustain if recent declines in gas prices continue to reverse course.”

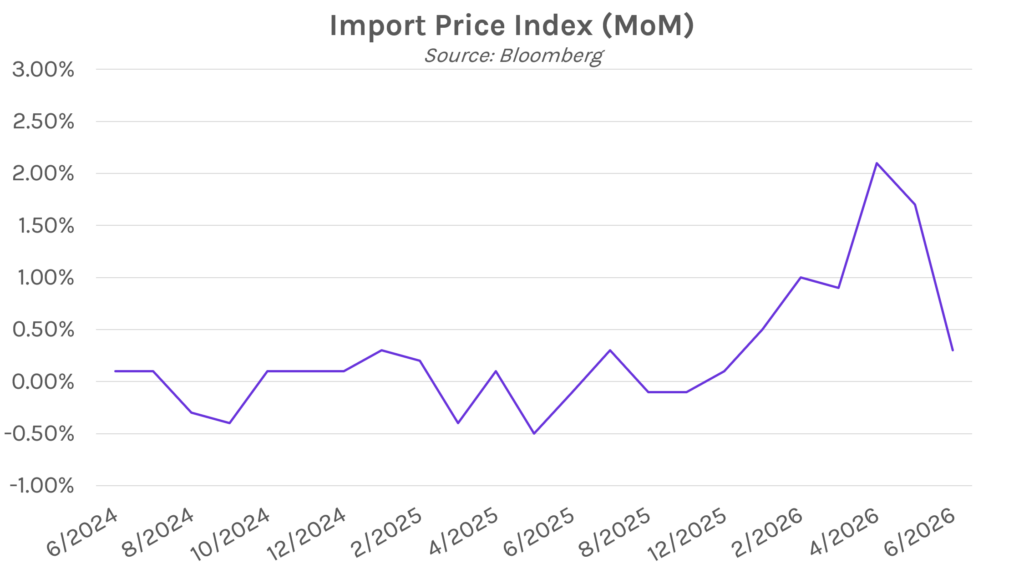

June import prices climb unexpectedly. Import prices rose 0.3% in June, well above expectations of a 0.7% decline but below May’s downwardly revised 1.7% increase. The annualized rate jumped to 7.1%, the largest increase since August 2022. The gain was driven by higher costs for capital and consumer goods and industrial materials, which more than offset falling energy prices. Prices for goods from China jumped 0.9%, the biggest monthly move since 2008 and a likely sign of tariff pass-through. Today’s report follows energy-led cooling in this week’s CPI and PPI data, adding uncertainty to the broader inflation outlook.