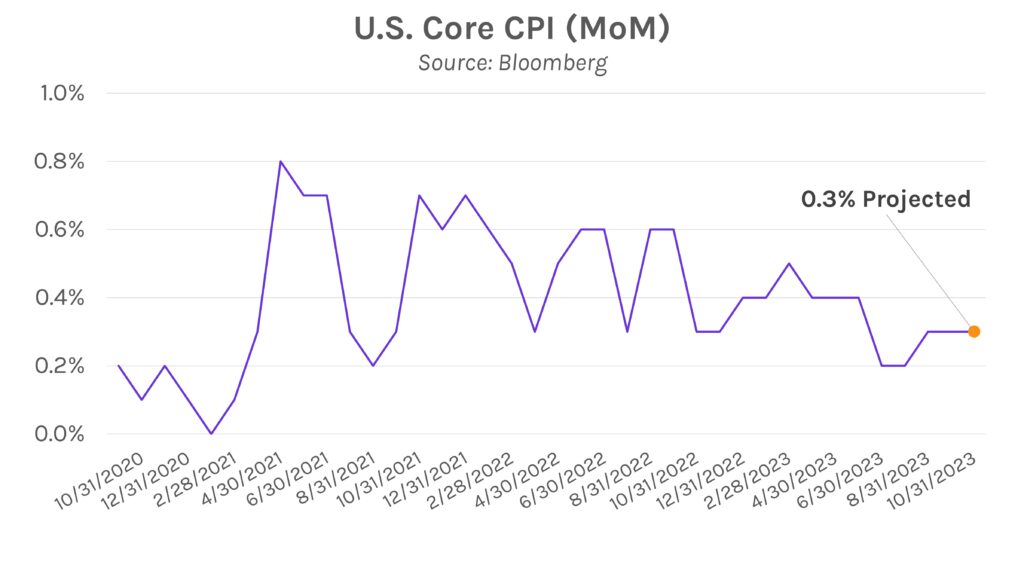

Rates fall ahead of CPI. Swap rates and US Treasurys were little changed ahead of tomorrow’s CPI data, where forecasts project a sharp decline in headline inflation but flat core prints. The short end of the yield curve declined as many as 3bps, while the long end ticked 1bp lower on the session. A soft print could spur talks of an early reduction to policy rates, which currently aren’t priced in until the end of 2024.

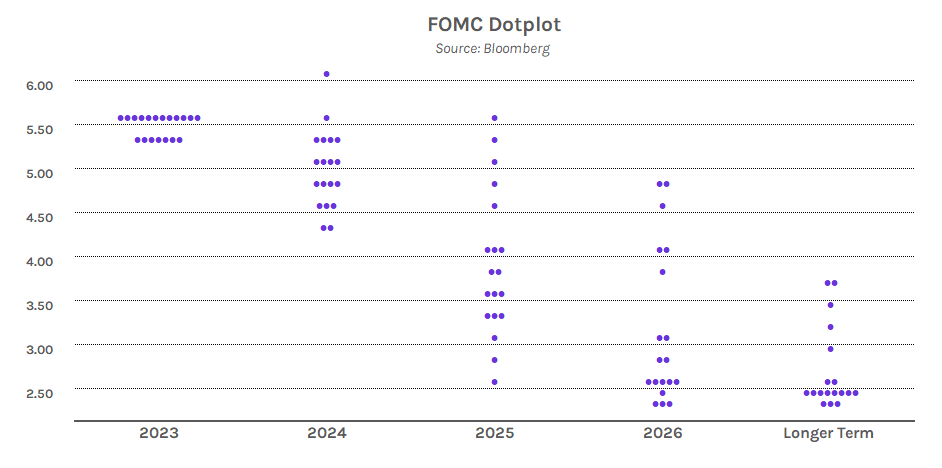

The path of future rate changes remains uncertain. Tomorrow’s inflation print could go a long way towards breaking the stalemate in interest rate markets. Ever sinceFed Chair Powell signaled a potential pause in rate hikes, the market has priced in low odds of any additional increases in the months ahead. However, predictions diverge on when rates could begin to decline. UBS and Morgan Stanley forecast that the Fed Funds rate will decline back to 2% by the end of 2025. In contrast, Goldman Sachs projects that the Fed Funds rate will remain at 4%. The Fed’s own projections call for Fed Funds to remain near 4%.

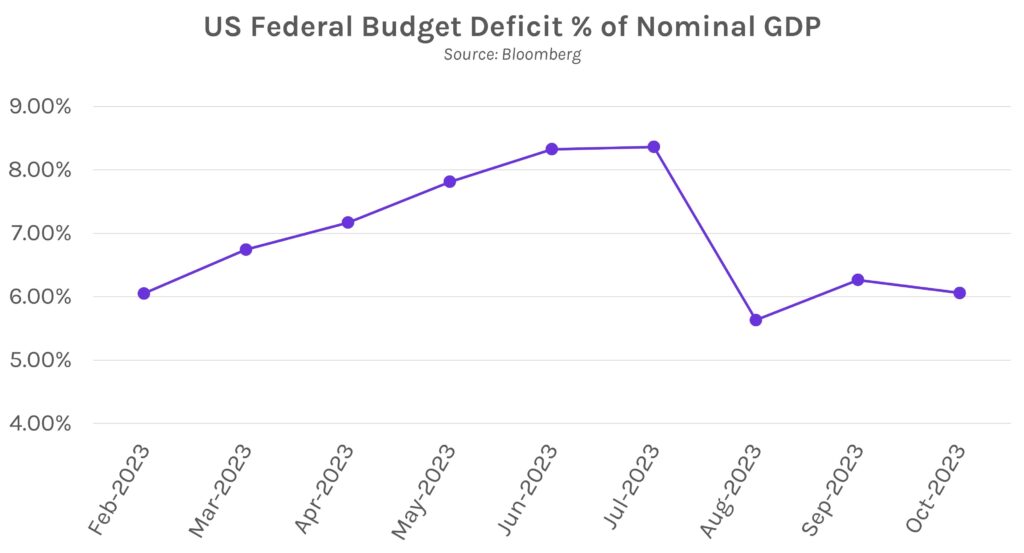

Cost of US Debt Soars. Interest costs on US debt climbed 87% in October on a YoY basis according to Treasury Department data released today, even as the monthly deficit shrank by 24% versus last October. Higher interest rates are the key contributor – the average rate on all outstanding US debt was 3.05% in October, the highest since 2010 and 87bps higher than last year. Though the US economy has remained strong, the ever-increasing deficit has prompted warnings from economists and ratings agencies; last week, Moody’s signaled it may revoke the US’ last remaining top credit rating from a major agency. These figures come amidst another government shutdown crisis due to gridlock over the federal budget. Funding runs out after November 17th.