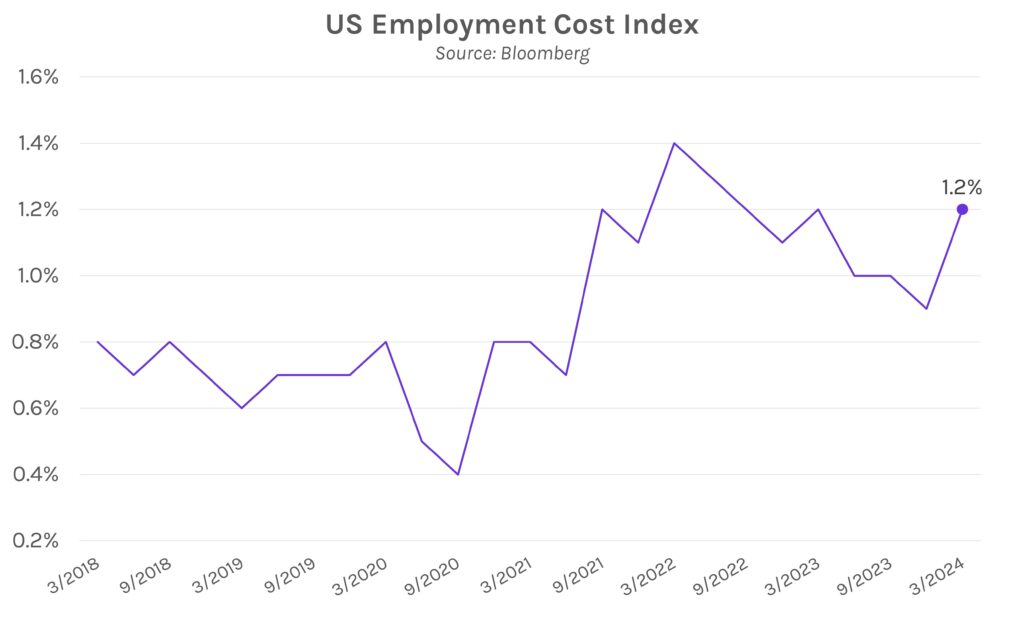

Higher than expected labor costs push rates 5-7bps higher. The employment cost index was 1.2% in Q1 versus the 1.0% estimate, which reinforced the notion that the Fed will approach any rate cuts with caution. Swap rates and UST yields immediately rose ~5bps after the data release and grinded higher throughout the afternoon. The 2y UST yield closed at 5.04%, the first close above 5% since November. The move came ahead of tomorrow’s FOMC decision, where the Fed is all but guaranteed to leave rates unchanged.

The Fed is almost guaranteed to hold rates steady tomorrow. Fed Funds futures suggest a 1% chance of a 25bp rate cut tomorrow and ~28bps of cuts in 2024. It’s a stark contrast from the beginning of the year, where 6-7 25bp rate cuts were seen as the baseline. A string of hot inflation figures drove the change, leading Chair Powell to say a few weeks ago that “it’s likely to take longer than expected to achieve that confidence.” Markets will peruse any forward-looking guidance that Chair Powell offers at his press conference.

Eurozone escapes recession, but inflation persists. Eurozone GDP increased 0.3% on a quarterly basis, the fastest in ~1.5 years, driven by faster economic growth in the bloc’s 4 largest economies. The news was reassuring after economic contraction during 2H23, and now the ECB expects overall economic growth of 0.6% in 2024 and 1.5% in 2025. Separately, inflation was 2.4% YoY, in-line with analyst estimates and steady with last month’s figures. Commenting on the inflation results, Europe economist at BNP Paribas Gerardo Martinez said that the first decline in services inflation in 6-months was a “more important development that increases our confidence that the ECB will lower policy rates in June.”