Underwater security portfolios and their impact on capital were among the causes of last year’s banking crisis, a sign of significant gaps in interest rate risk management, according to Fed Vice Chair for Supervision Michael Barr. Treasury Secretary Janet Yellen argued last week that banks must maintain “diverse sources of contingency funding,” which would help to prevent capital losses from security sales. Although no formal changes have been made, it appears regulators may limit the extent to which larger banks can rely on held-to-maturity (“HTM”) securities in liquidity buffers and stress tests.

Regardless of the asset size of an institution, higher regulatory scrutiny surrounding HTM securities, liquidity, and capital makes interest rate hedges a key tool to protect against losses in higher rates.

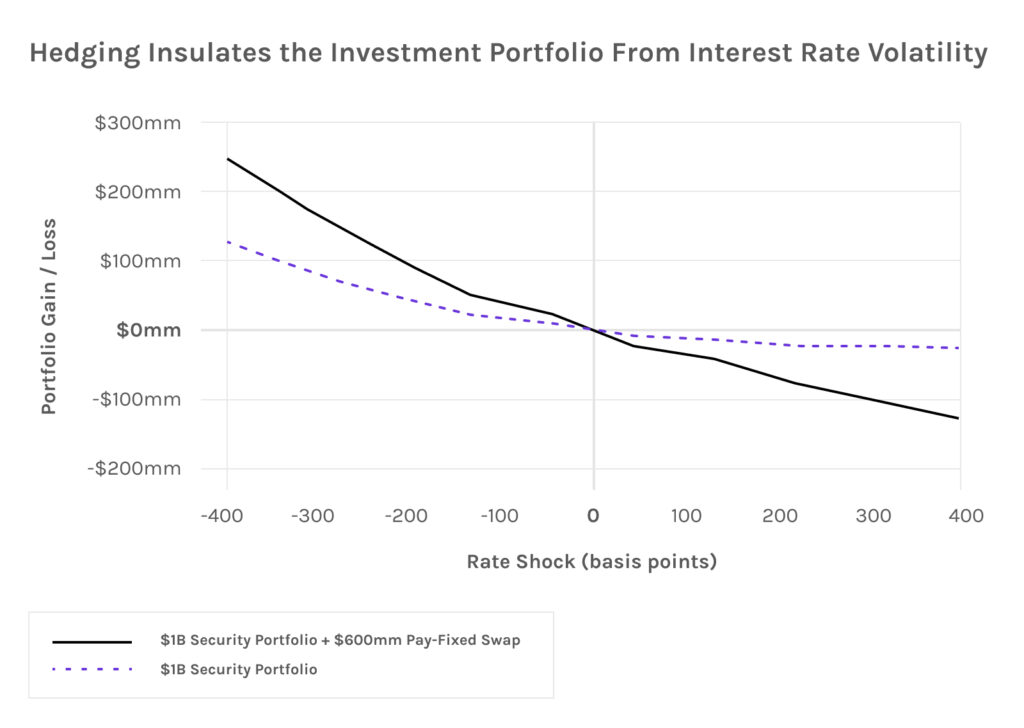

Depositories can execute pay-fixed swaps to offset losses in the investment portfolio. Under hedge accounting, fair value hedges like pay-fixed swaps impact other comprehensive income. As can be seen below, swaps can reduce the sensitivity of the investment portfolio to interest rates and preserve the portfolio as a source of liquidity:

Pay-fixed swaps designated against pools of fixed-rate securities are eligible for fair value hedge accounting under the portfolio layer method (PLM). With PLM, any fixed-rate available-for-sale (AFS) security can be included in the hedged pool and remain unencumbered. Securities can be sold or pledged without penalty provided that the pool balance matches or exceeds the swap notional. Recent enhancements to PLM mean that shortfalls in pool balance (below the swap notional) result in a loss of hedge accounting on only the shortfall amount. Furthermore, PLM now allows for multiple hedges to be designated against the same pool, limiting concerns about overcollateralizing the asset pool.

The 2023 banking crisis underscored the importance of protecting capital against interest rate volatility. Pay-fixed swaps can be used to hedge potential losses and ensure that financial institutions are able to meet capital and liquidity requirements. Please contact us at if you have any questions.