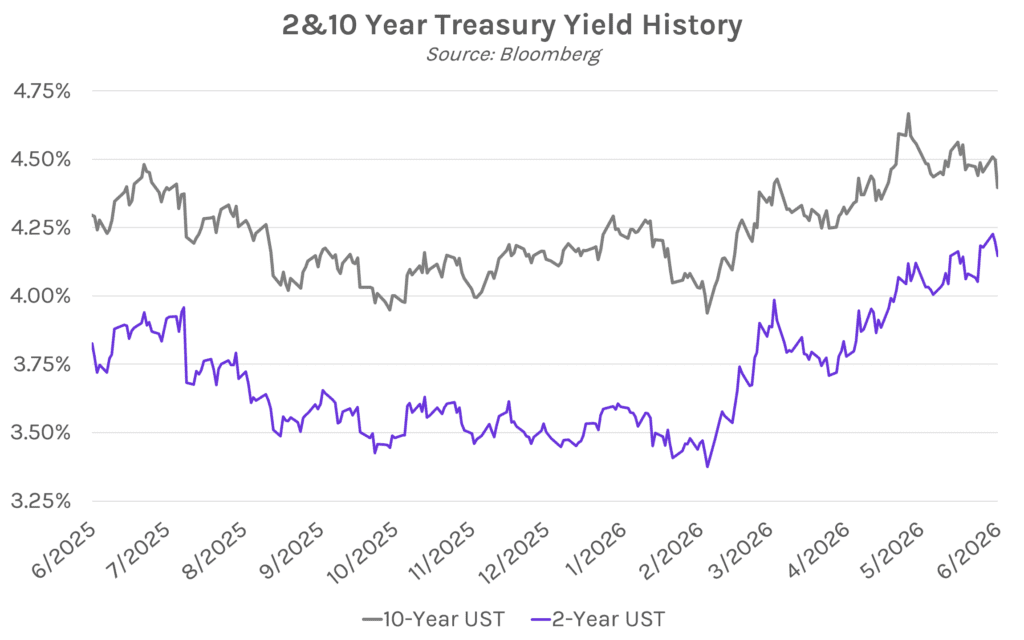

Yields fall on easing oil prices. Treasury yields declined as oil prices continued to retreat, with increased vessel activity in the Strait of Hormuz alleviating concerns over energy-driven inflation. The 2-year yield closed 5 bps lower at 4.15% and the 10-year yield closed 11 bps lower at 4.39%. Oil prices are now near pre-war levels, with WTI at $70 per barrel and Brent at $73 per barrel. Meanwhile, equities are climbing in after-hours trading following a strong earnings outlook from Micron Technology, though the S&P 500 and NASDAQ closed 0.10% and 0.43% lower today, respectively.

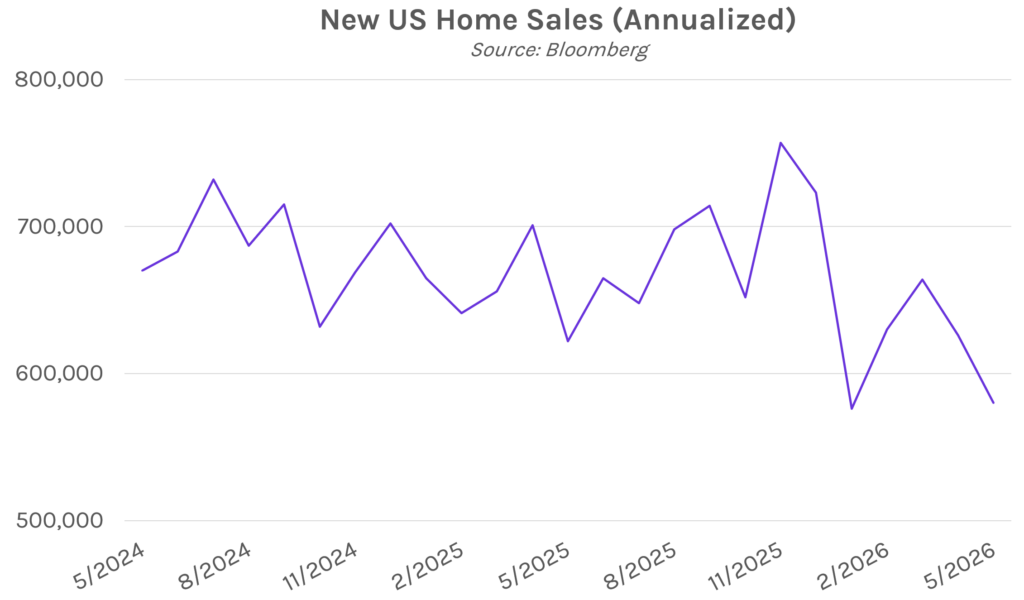

New home sales fall to lowest level since January. Sales of new single-family homes fell 7.3% in May to an annualized rate of 580k, well below estimates of 640k and April’s 626k. Marking the lowest level since the beginning of the year, the decline was largely driven by elevated mortgage rates and home buyer affordability concerns. Homebuilders continue to offer incentives such as price cuts and mortgage payment subsidies in an effort to entice buyers. In May, the supply of new homes available in the US fell 1.4% YoY, however the 496k available homes still represent a 10.3 month supply at the current sales rate, matching the highest level since 2009.

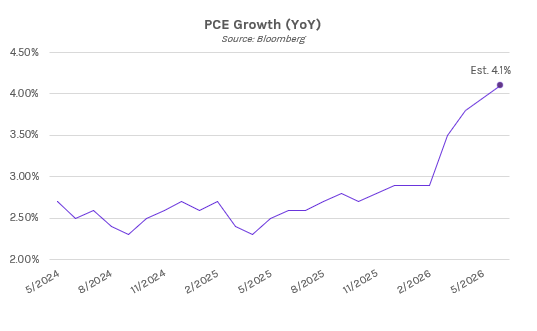

May PCE expected to show inflation ticked higher. PCE data due tomorrow is expected to show headline inflation rose 0.5% MoM in May, up from 0.4% in April. Core PCE, which excludes food and energy prices, is expected to rise 0.3% MoM and 3.4% YoY, versus 0.2% and 3.3%, respectively, in April. Tomorrow’s report is unlikely to capture the oil price relief seen in recent weeks. While crude prices have now fallen back to pre-war levels, any relief will likely take time to flow through to the data. As the Fed’s preferred inflation gauge, the release is likely to draw particular attention following last week’s hawkish FOMC statement and policymakers’ continued inflation concerns.