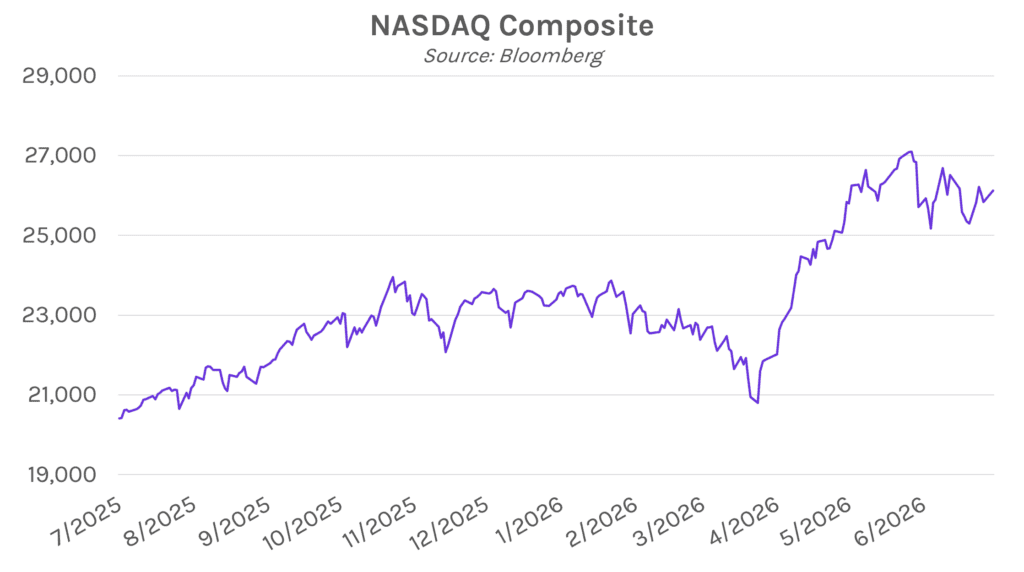

Yields drift lower despite steady ISM print. Treasury yields traded in a tight 2-3 bp range over the course of a quiet post-holiday session, as markets largely looked past today’s ISM services data report. The 2-year yield closed 3 bps lower at 4.11%, while the 10-year yield closed 1bp lower at 4.47%. Meanwhile, equities climbed as renewed excitement for AI drove technology stocks higher, with the S&P 500 and NASDAQ closing 0.72% and 1.12% higher, respectively.

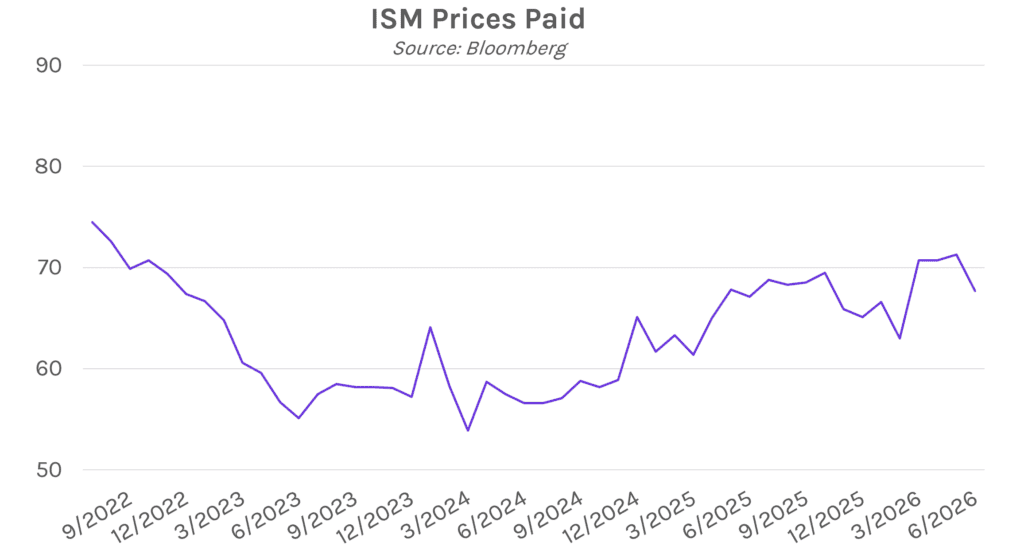

Services activity expands as prices paid, new orders fall. US services activity held in expansionary territory for the 24th consecutive month in June, with the headline ISM services index coming in at 54.0, down slightly from 54.5 in May but in line with expectations. Fourteen industries reported growth, while four sectors contracted, including agriculture and educational services. The measure of prices paid fell to 67.7 from 71.3, dropping below 70.0 for the first time since February but still above estimates of 67.5, suggesting services inflation, while easing, has further to go. New orders also softened, falling to 55.1 from 57.3 in the prior period, which could provide further inflationary relief in the months ahead.

Fed’s Waller pushes back on scrapping forward guidance. Fed Governor Christopher Waller made the case that forward guidance remains a valuable policy tool as new Chair Kevin Warsh looks to phase it out. Waller argued the tool can speed the transmission of monetary policy by shaping market expectations, but conceded it must be used carefully, saying it is “more art than science, and there have been times when it has hindered, rather than helped, policymaking.” He pointed to 2020 and 2021 as a cautionary case, when guidance issued in September 2020 went unchanged as inflation climbed and unemployment fell, leaving officials to feel constrained from acting.