While the forward curve gets most of the attention, option prices can provide Banks and Credit Unions unique insights into the distribution of potential rate outcomes.

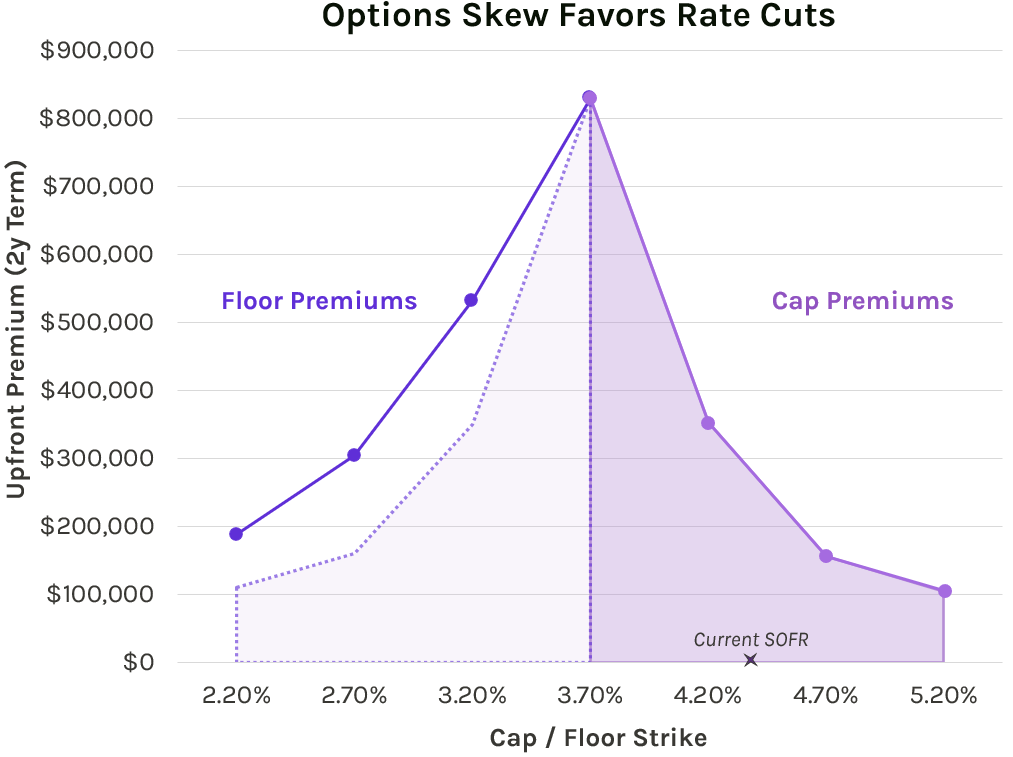

Theoretically, caps and floors with equally out-of-the-money strikes should have the same price. However, in reality, buyers and sellers recognize that the distribution of rate outcomes is not normally distributed and accordingly “skew” the pricing of caps or floors higher. Skew can be thought of as an additional premium for specific rate scenarios.

In today’s market, floors are priced at a significant premium to caps, even after adjusting for the inverted curve. Currently, the options-implied probability of a 300bp move lower in rates is the same as the probability of a 100bp move higher in rates over a two year period. A 100bp out-of-the-money floor costs double the premium of a 100bp OTM cap:

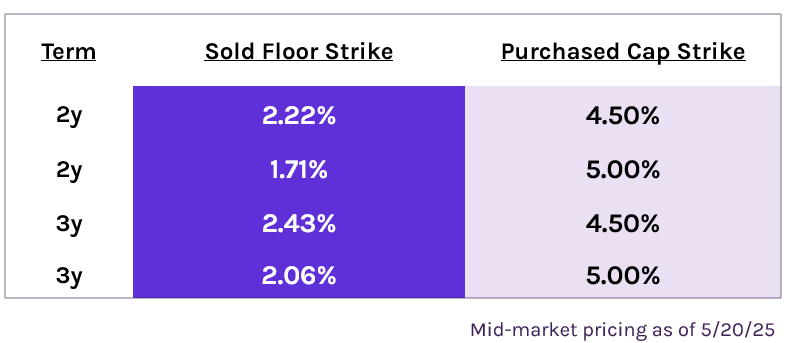

Costless Collars

For banks and credit unions with earnings exposure to rising rates, a costless collar monetizes the premium in floor pricing and uses those proceeds to buy a cap. The structure results in a cap struck substantially closer to current rates than the sold floor. Under a costless collar structure, banks receive payments when rates rise above the cap strike, and make no payments until rates decline below the sold floor strike. We’ve included pricing for several structures below:

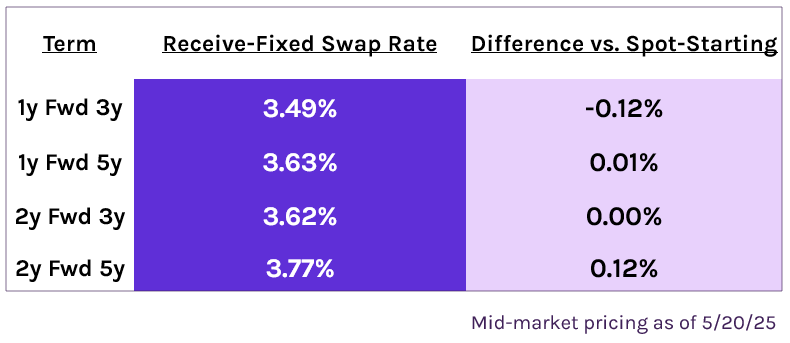

Forward Starting Receive-Fixed Swaps

Banks and credit unions with exposure to lower rates should also take note of the skew in the options market. The skew speaks not only to the likelihood of rate cuts but also the potential speed of a move lower. While floors remain useful for institutions needing one way protection, forward-starting receive-fixed swap pricing has started to look attractive given the recent steepening in the curve:

Revisit our recent pieces:

- Strategies from Q1 Earnings Calls Part I & Part II

- Hedging Through the Tariff Storm

- No Free Lunch

- Webinar Replay: Regulatory Reporting for Hedging Programs